1 year ago

52

1 year ago

52

Key events

In France, household confidence slipped slightly in March.

According to the economics institute Insee (Institut national de la statistique et des études économiques), its monthly indicator dropped one point to 81 in March and remained well below its long-term average of 100 between 1987 and 2022.

Households’ balances of opinion on their future and past financial situation are stable, as is the one on major purchases intentions, all three remain well below their long-term average.

The share of households considering it is a good idea to save has fallen again after a sharp increase in February. The balance of opinion has declined four points but remains well above its long-term average.

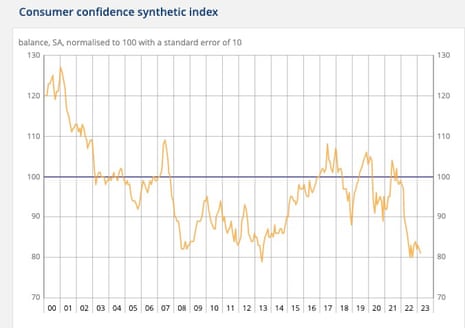

In Germany, consumer confidence continues to improve as energy prices ease, although a full recovery is still some way off.

The GfK institute’s closely watched index recorded an unexpected rise to -29.5 going into April, from a revised reading of -30.6 in March. Markets had expected a drop to -33.1.

April’s rise is the sixth monthly improvement in a row, but the pace has slowed noticeably compared with previous months.

GfK consumer expert Rolf Buerkl said:

The anticipated loss of purchasing power is preventing a sustained recovery of domestic demand.

This is also indicated by the still very low level of consumer confidence.

The income outlook is currently benefiting from noticeably lower prices for energy, especially for gasoline and heating oil. Nevertheless, inflation will remain high.

The subindex measuring income expectations was the main contributor to the increase in sentiment, rising to its highest level in 10 months.

European stocks have opened slightly higher, the third day of gains.

The UK’s FTSE 100 index is up 21 points, or 0.3%, to 7,506, while Germany’s Dax and France’s CAC rose 0.7%, and Spain’s Ibex and Italy’s FTSE MiB advanced 05%.

The pound has slid 0.2% against the dollar to $1.2313.

Victoria Scholar, head of investment at the trading platform interactive investor said:

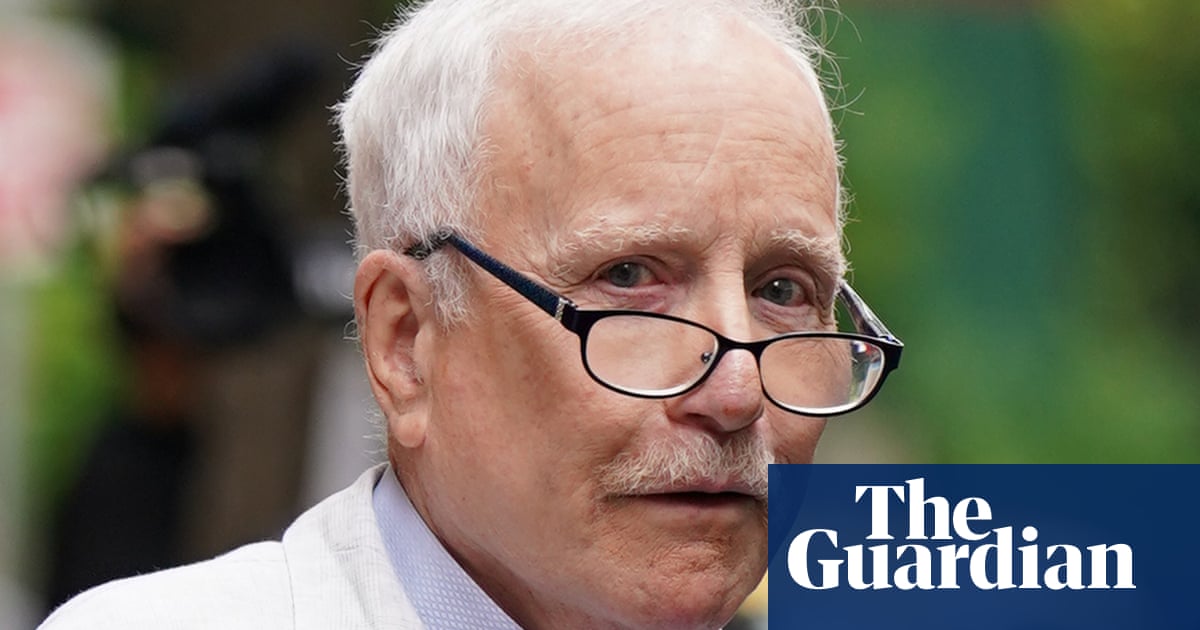

Ermotti previously served as chief executive of UBS from 2011 until 2020 and is currently the chairman of Swiss Re. Ralph Hamers who has been in the top job since November 2020 is stepping down ‘in light of the new challenges and priorities facing UBS’. Ermotti said ‘the task at hand is an urgent and challenging one’.

Having steered UBS through the aftermath of the 2008 global financial crisis and a rogue-trading scandal, Ermotti is a dab hand at crisis management. He also helped UBS to navigate through the onset of the pandemic and the corresponding market volatility throughout most of 2020.

The new CEO will have the immediate challenges of cutting staff, reducing Credit Suisse’s investment bank, finding other synergies between the two lenders and convincing shareholders about the prospects of the combined entity.

Introduction: UK chain Next expects to raise prices more slowly; UBS appoints new CEO to steer Credit Suisse takeover

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

Some calm has returned to stock markets and European markets notched up some modest gains yesterday but struggled for direction.

The UK high street chain Next has said it expects to raise its prices more slowly over the year ahead as it revealed better-than-expected annual profits of £870m.

Like-for-like price inflation in the spring and summer collections is expected to be +7% and, in the autumn/winter, +3%, down from +8% and +6% respectively.

We now believe price rises in the second half will be materially lower than we initially feared.

Next cited a significant reduction in the cost of container freight as shipping capacities return to normal, as well as improving factory gate prices (the price at which it purchases the goods in the country of origin). The majority of these benefits will be felt in the second half of the year.

In a surprise move, UBS has brought back its former boss Sergio Ermotti and appointed him as chief executive, to steer its massive takeover of Credit Suisse.

He will replace the current CEO Ralph Hamers on 5 April. Hamers, who succeeded Ermotti in November 2020, will stay on as adviser during a transition period, Switzerland’s largest bank said in a statement.

Ermotti previously ran the bank for nine years and oversaw a restructuring of the investment bank. UBS said:

This unique experience, together with his deep understanding of the financial services industry in Switzerland and globally, make Sergio Ermotti ideally placed to pursue the integration of Credit Suisse.

The move comes less than two weeks after UBS agreed to take over Credit Suisse in a in a £2.65bn deal forced through by Swiss authorities who feared that a failure to protect depositors would trigger a global banking meltdown.

Here’s an old tweet from Tracy Alloway, co-host of Bloomberg’s Odd Lots podcast:

Ermotti said:

The task at hand is an urgent and challenging one.

In order to it in a sustainable and successful way, and in the interest of all stakeholders involved, we need to thoughtfully and systematically assess all options.

The task involves combining two banks with $1.6 trillion in assets, more than 120,000 staff and a complex balance sheet. Hamers has no big M&A experience.

Later this morning, we will get lending data from the Bank of England that will give an insight into the state of the UK housing market and consumer lending more generally.

Michael Hewson, chief market analyst at CMC Markets UK, said:

UK mortgage approvals have seen a sharp slowdown in the last few months as higher interest rates and the rising cost of living serves to crimp demand, even as the lead-up to Christmas tends to see a slowdown in demand.

In January mortgage demand fell to its lowest level since 2020 at 39.6k, and today’s February numbers aren’t expected to see a significant pickup with expectations of around 40k.

In January net consumer credit saw a sharp pickup to £1.6bn, after a slowdown at the end of last year that saw consumer borrowing slow to £800m from £1.5bn. This stop start nature of consumer borrowing points to a UK consumer that is very sensitive to the rising cost of living, and while consumer confidence has improved in recent months it remains very fragile.

Today’s consumer credit numbers for February are expected to show a modest slowdown to £1.2bn, with recent trends in retail sales showing that discretionary demand has started to pick up as energy prices have fallen back.

The Agenda

9.30am BST: Bank of England Mortgage approvals and consumer credit for February

9.45am BST: MPs on Treasury committee grill Jeremy Hunt on spring budget

10.30am BST: Bank of England Minutes of financial policy committee meeting

2pm BST: Swiss National Bank Quarterly bulletin

3pm BST: Federal Reserve vice-chair for supervision, Michael Barr, testifies on SVB collapse

English (US)

English (US)